The End of [Entire Fairness] As We Know It?

Preview of In re Match Group, Inc. Derivative Litigation, No. 368, 2022, hearing (Del. Dec. 13, 2023) and a comeback from hiatus.

The Chancery Daily x Substack is devoted to deep dives on popular matters in the Delaware Court of Chancery and other Delaware courts. When cases like Twitter v. Musk, Fox v. Dominion, or In re AMC Entertainment Holdings, Inc. are going on (and on and on and on and on), this Substack publishes regularly, sometimes even multiple times per day. I put my heart and soul into sharing all the relevant things about those kind of popular interest cases with this audience, because I truly give a fck. When such cases calm, and the waters quiet, I take hiatuses where I can.

The last few months have been one such much-needed hiatus, but it’s time to ramp up production here once again. For those of you who don’t know, The Chancery Daily’s main publication is The Long Form, which is a trade publication geared toward lawyers and practitioners in the Delaware Courts, and of which I am the Editor-in-Chief. The Long Form is also subscribed to by some sophisticated finance types, and many academics. We even have a few hard-core legal geeks on our rolls.

As you should know, I don’t post on Twitter (alav ha-shalom), but if you want to follow my random thoughts of the sort that used to go there, you can follow me on Threads. It’s mostly jokes, memes, and quirky random thoughts on all things legal, tech, and the morass that is Musk’s absolute destruction of $44 billion, his reputation, and the platform that used to be found at twitter dot com. Threads is actually a great platform, and it’s nearly Nazi free, which is more than I can say for the old place.

By way of brief update on what you can expect to see in future Substack posts here, there are many cases of public interest pending in the Delaware Court of Chancery at the moment, including but not limited to:

Elon Musk’s compensation case concerning $55 billion in option grants, Tornetta v. Musk is pending post-trial ruling after post-trial supplemental briefing was completed.

Tesla’s director compensation settlement, in Police and Fire Retirement System of the City of Detroit v. Elon Musk, et al. which was subject to objection, is pending a ruling from the fairness hearing.

Briefing in the AMC Entertainment appeal at the Delaware Supreme Court (no, not this one, the Rose Izzo appeal) is soon to be filed, and will be scheduled for oral argument once briefing is complete. (Yes, it’s really not over!)

The Sjunde AP-Fonden v. Activision Blizzard, Inc. case is pending a ruling on motions to dismiss, for summary judgment, and to stay.

The currently-stayed remedies trial in 26 Capital Acquisition Corp., et al. v. Tiger Resort Asia Ltd., et al., C.A. No. 2023-0128-JTL, which is now pending the outcome of Rimu Capital Ltd v. Ader, C.A. No. 2023-1109-JTL.

The inevitable showdown that will come to a head someday concerning the former Twitter execs’ owed parachute payments.

Updates from the Match Group oral argument on December 13, 2023 at the Delaware Supreme Court.

Goings on in recent cases filed in the Court of Chancery involving Disney, WWE, Netflix, NVIDIA, and many others.

Whatever else readers might request coverage on! Go ahead, reply to this email, I dare you.

Most of these posts on Substack will be for paying subscribers, but there is always a significant amount of free content for those of you with only a passing interest. We’re glad you’re here — whether you are a die-hard or a newbie.

But today, I’d like to bring you some cross-over content from our flagship publication about an incredibly important case that has been working its way through the Delaware Courts, and is on tap for oral argument at the Delaware Supreme Court on December 13th. The below synopsis was prepared for lawyers, so pardon its somewhat more sophisticated language, and its lack of background deep dives on all the new concepts it’s touching on. But it’s important, and some of you will take what you can, and the rest of you will ask great questions in the comments, and everyone will learn and grow!

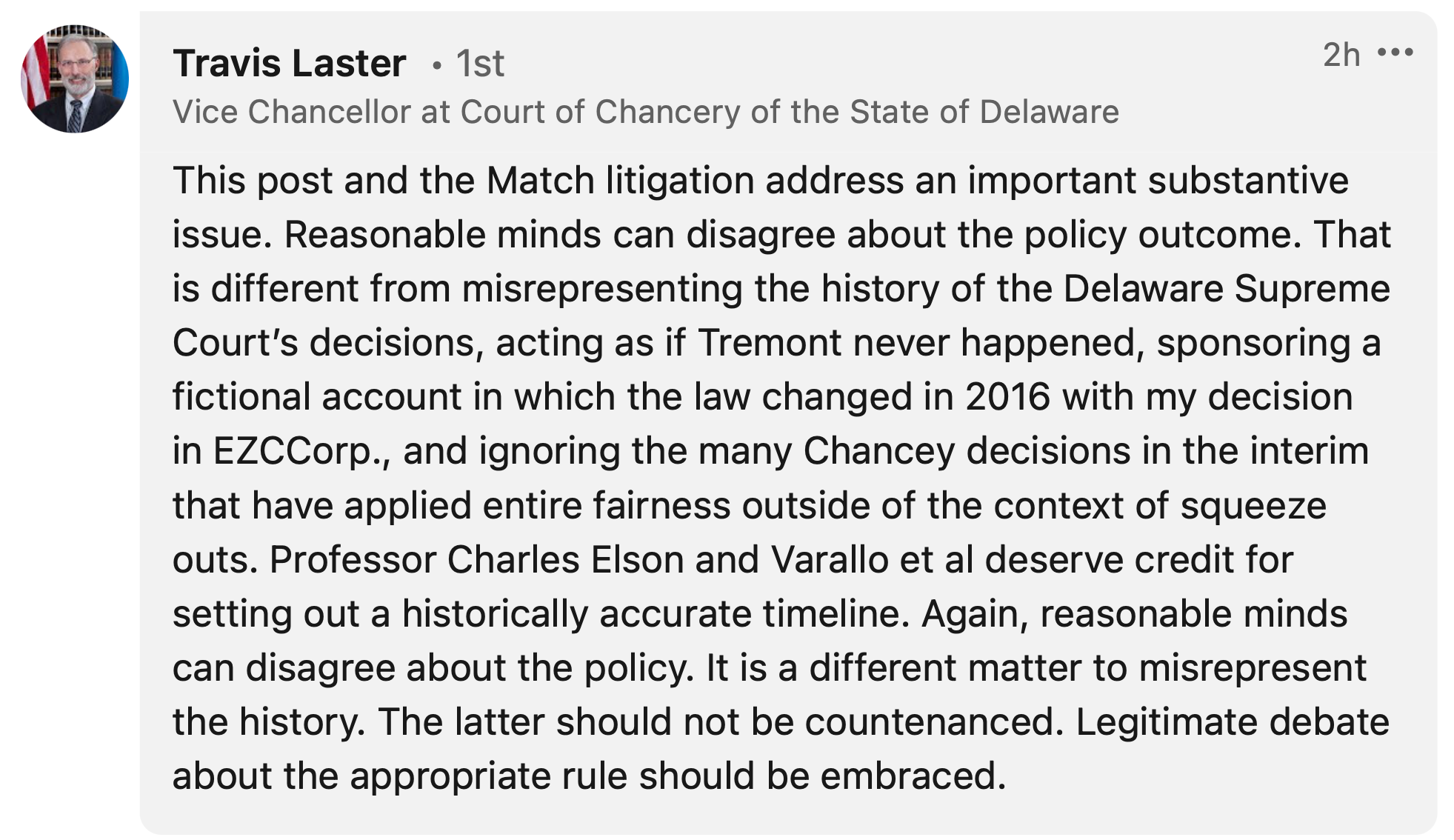

Much commentary has been written on the topic of the In re Match Group, Inc. Derivative Litigation appeal, including a recent piece from Gregory Varallo, Andrew Blumberg, and James Janison of Bernstein Litowitz entitled “Optimizing” and Match: Bad Policy Threatens to Drive Bad Law. That piece even got a response on LinkedIn from the Honorable Vice Chancellor Laster himself that gives more than a hint of his take on the certain positions argued by defendants in the case:

If it’s not clear, those are strong words. But after our entire team took a deep dive on all of the Match briefing, I can say with confidence that they are entirely justified. The question is whether or not the Delaware Supreme Court will be snowed by arguments that seem nearly dependent on thinking that the Justices are something other than what they are — some of the smartest, sharpest, insightful minds in the state. Inshallah they will see rightly.

You can read our Long Form diegesis of the entire Match case and what’s at stake here, where you can also find links to all the cases and briefing, and our summary of all the arguments that have been put forth. For those of you who don’t like clicking links, you can simply read on below for the take-away. This is an important case that threatens to significantly alter certain protections for minority stockholders, which have traditionally been — in my humble opinion — the hallmark of the Delaware franchise. I have talked before about my mentor Professor Michael Wachter, and I went back and checked my Corporations outline, and I wasn’t going crazy (at least not like that) when I was reading defendants’ arguments and found them to be nearly antithetical to the propositions I have always known to be true about how Delaware law works. Kahn v. Tremont is in my outline, for exactly the proposition that I thought it stood for, in the non-squeeze-out merger context — that “[o]rdinarily, in a challenged transaction involving self-dealing by a controlling shareholder, the substantive legal standard is that of entire fairness, with the burden of persuasion resting upon the defendants” and moreover, that use of a single protection (such as — in that case — a special committee) does not alter the burden of proof, much less the standard of review. Now, of course, things have changed and the law has evolved since 1997, but as you can see from VCL’s comments above, defendants’ arguments don’t seem to get any more tethered to reality when covering the intervening years.

I’ve written before about how it’s hard to speak (what I see as) the truth publicly, given my great respect for many of the lawyers involved in any given case in Delaware. It’s a small bar. I will see these people at conferences, I enjoy talking inside baseball with them. The Delaware Way, though I love aspects of it, sometimes treads dangerously close to silencing dissent and real talk about matters of importance. But whereas some people consider lawyers who practice in Delaware to be thin-skinned enough to hold it against me if I speak out on what I believe is right, I like to see them as bigger people who wouldn’t be so easily frayed. The law is all about debate and the different ways that the same truth can be conceived of, and although I don’t have a dog in the fight, I nonetheless advocate for what I think is right. And regardless of how people feel about it, I will share my view, and they can share theirs. And hopefully, we can have lively and educated debate about the legitimate issues at play in any given instance. And I’m always up for being proved wrong, or having my mind changed about things. I have spent my whole life learning, I’m not about to stop now.

Much love, as always —

Chance

Striving to better, oft we mar what’s well.

William Shakespeare, King Lear (1606)

Today’s edition of The Chancery Daily previews arguments on appeal in advance of oral argument in In re Match Group, Inc. Derivative Litigation, No. 368, 2022, hearing (Del. Dec. 13, 2023), which we perceive to be of great significance. Given its importance, we are sending this special edition of The Long Form to our free and paid subscribers of all stripes. If you want to receive this kind of analysis and in-depth coverage on a daily basis, reach out for more information on how to subscribe.

TCD reiterates disclaimers that arguably have been watered down by repetition over the years, but which nevertheless remain always true and relevant to our presentation. We do not represent parties in litigation. We report what happens in litigation without allegiance to what could be characterized as plaintiff-friendly or defendant-friendly legal rules or outcomes. To the extent we have any preference on litigation outcomes, it is that Delaware law will be rendered with integrity to achieve just results -- consistent with its deep roots in the equitable tradition -- and that it will thus remain justifiable as an influential de facto national body of corporate law.

Not coincidentally, this publication’s namesake institution has, for more than a century, honed unparalleled expertise and a unique body of corporate law based on equity – and is thus adaptable to address injustice. It is that body of law that distinguishes Delaware and has elevated it among all other jurisdictions as a preeminent forum for business entity formation and business dispute resolution. Less well-known but of greater societal significance is Delawarean equity’s contribution to matters of social justice. See Ethel Louise Belton, et al. v. Francis B. Gebhart, et al., C.A. No. *258-CS, opinion (Del. Ch. Apr. 1, 1952), affirmed sub nom. Oliver Brown, et al. v. Board of Education of Topeka, et al., No. 1, opinion (U.S. May 17, 1954). Indeed, this publication was intended not only to assist counsel in practice before the Court of Chancery, but to promote awareness of and respect for Delaware’s influential equity-infused law. Our quasi-labor of love was fostered by the views that equity well serves the ends of justice -- and that Delaware’s just law contributes significantly to macro-level stability of the U.S. economy. Such is TCD’s view of equity’s paramount importance to Delaware law.

Perhaps somewhat ironically then, shortly after TCD’s launch in 2012, Delaware law began to constrain the role of equity. Significantly, in the Supreme Court’s decision in Alan Kahn, et al. v. M&F Worldwide Corp., et al., No. 334, 2013, opinion (Del. Mar. 14, 2014), the High Court adopted a novel mechanism by which the judicial standard of review of interested controlling stockholder mergers would shift from entire fairness to business judgment if a transaction was structured using procedural “protections” in the form of approval by both an independent committee and a majority of minority stockholders. The novelty was to shift thestandard of review, as opposed to merely shifting the burden of proof for demonstrating that a squeeze-out merger was or was not entirely fair from a controlling stockholder to minority stockholders, as occurs under Alan R. Kahn v. Lynch Communication Systems, Inc., et al., No. 272, 1993, opinion (Del. Apr. 5, 1994) when only one of the “protections” is used. Standard shifting, rather than burden shifting, was provided as an inventive tool to encourage controllers to use both stockholder-protective mechanisms.

Following M&F Worldwide, the Supreme Court issued Robert A. Corwin, et al. v. KKR Financial Holdings, LLC, et al., No. 629, 2014, opinion (Del. Oct. 2, 2015), which conceptually followed M&F Worldwide by providing for case-dispositive standard shifting, albeit in non-controlling stockholder transactions. Under Corwin, “when a transaction not subject to the entire fairness standard is approved by a fully informed, uncoerced vote of the disinterested stockholders, the business judgment rule applies,” and, as a practical matter, the action will be dismissed. Corwin differed from M&F Worldwide in that the basis for standard shifting was not to incentivize use of procedural protections, but because stockholder voting was deemed to have “cleansed” the transaction through ratification. But the result of standard shifting under both M&F Worldwide and Corwin would be the same: challenged transactions would be placed beyond equitable review of the Court.

As TCD discussed at some length in its January 6, 2023 edition, the concept of standard shifting under M&F Worldwide was conceived as a means of stockholder protection. As articulated in two pre-M&F Worldwide decisions (In re Cox Communications Shareholders Litigation, C.A. No. 613-VCS (consol.), opinion (Del. Ch. Jun. 6, 2005) and In re MFW Shareholders Litigation, C.A. No. 6566-CS (consol.), opinion (Del. Ch. May 29, 2013)), approval by both an independent committee and a stockholder vote would replicate an arms-length bargain in a transaction between a controller and a controlled company, which would both protect stockholders from misappropriation of corporate value by the controller -- by ensuring the best price (at least hypothetically) -- and protect fiduciaries from meritless lawsuits by shifting the standard of review to business judgment, requiring dismissal; to the extent the procedural protections failed to protect stockholders from value misappropriation and ensure the best price, statutory appraisal provided a backstop. The M&F Worldwide Court’s adoption of the standard proposed in the In re MFW decision modified the policy rationale, however, in emphasizing stockholder protection against misappropriation of value by the controlling stockholder and making no reference to preclusion of non-meritorious claims or accrual of settlement value by facilitation of pleading-stage dismissal. The “protection” that drove the M&F WorldwideCourt’s decision was solely protection of stockholders.

As TCD has noted, the standard adopted by the M&F Worldwide Court is materially different from the standard articulated by the In re MFW Court, and it is in no small sense confusing that both the M&F Worldwide decision and the standard it announced are routinely described as “MFW.” The standard should probably be called the Synutra standard because, as discussed in our January 26, 2023 edition, the Supreme Court’s subsequent decision in Arthur Flood v. Synutra International, Inc., et al., No. 101, 2018, opinion (Del. Oct. 9, 2018) recontextualized the standard as one intended to avoid judicial review, and overruled the M&F Worldwide decision (which it refers to as “MFW”) to the extent that it was inconsistent with the Court of Chancery’s In re MFW opinion (which it also refers to as “MFW”). See footnote 81. The protection that drove the Synutra decision was protection of the controller. (Notably, by the time the SynutraOpinion overruled the M&F Worldwide Opinion’s allowance for equitable review of the value stockholders received in a controlling stockholder squeeze-out, the ability of stockholders to challenge the merger price through statutory appraisal -- touted particularly by the Cox Communications Court, and to a lesser degree by the In re MFW Court as a backstop protection -- was severely truncated by DFC Global Corp. v. Muirfield Value Partners, LP, et al., No. 518, 2016, opinion (Del. Aug. 1, 2017), Dell, Inc. v. Magnetar Global Event Driven Master Fund, Ltd., et al., No. 565, 2016, opinion (Del. Dec. 14, 2017), and Verition Partners Master Fund, Ltd., et al. v. Aruba Networks, Inc., No. 368, 2018, opinion (Del. Apr. 16, 2019)).

Corwin, for its part, introduced a unique procedural anomaly. Ratification, the basis for Corwin's vote-based standard shifting, is an affirmative defense that must be pled in an answer; yet the standard-shift to business judgment provided a pleading-stage basis for dismissal. In In re Solera Holdings, Inc. Stockholder Litigation, C.A. No. 11524-CB (consol.), memo. op. (Del. Ch. Jan. 5, 2017), the Court of Chancery ruled that, although defendants bear the burden of proof in showing that the criteria for a ratification defense are met, plaintiffs bear the burden of pleading facts in their complaint demonstrating that a stockholder vote was uninformed or coerced. In effect, this required that plaintiffs plead evidence required to overcome an affirmative defense that defendants would presumably assert in an answer, where no answer was filed, on a motion to dismiss, with no entitlement to discovery. TCD hesitates to say that this procedural anomaly is unique in the U.S. legal system, but we are aware of no analog. Although Solera dealt only with claims subject to a Corwinratification defense, the same procedural anomaly presumably applied to an M&F Worldwide “procedural protections” defense: a plaintiff must plead evidence.

The problem of pleading evidence without discovery led to other innovations, including pursuit of statutory appraisal to obtain discovery that might support a breach of fiduciary duty claim (which was curtailed to a degree by statutory amendments limiting stockholders’ entitlement to seek appraisal), and inspection of corporate books and records under 8 Del. C. § 220. TCD believes that the first action that sought books and records to plead around a Corwin defense was Elizabeth Morrison v. Fresh Market, Inc., C.A. No. 12243-VCG, compl. (Del. Ch. Apr. 22, 2016). That effort failed when the Court rejected plaintiffs’ argument that the stockholder vote was not fully informed in Elizabeth Morrison v. Ray Berry, et al. [Fresh Market], C.A. No. 12808-VCG, letter op. (Del. Ch. Sept. 28, 2017), and dismissed the matter as an "exemplary case" for application of Corwin. But oddly, on appeal, the Supreme Court, in Elizabeth Morrison v. Ray Berry, et al. [Fresh Market], No. 445, 2017, opinion (Del. July 9, 2018), undertook what one might consider an uncharacteristically searching review of evidence on review of a motion to dismiss -- most notably email from the non-controlling founder / director of the target company -- to reach a shocking conclusion: the non-controlling founder / director of the target company lied to the board with respect to material facts, resulting in the stockholder vote being uninformed.

As TCD observed in its Labor Day Weekend 2018 edition, “Fresh Market might be viewed as an initial success or proof of principle of the use of a ‘post-Corwin 220 action’ as a ‘tool at hand’ for obtaining information, pre-filing, supporting class action claims capable of withstanding dismissal . . . Fresh Marketcould foreseeably also be a catalyst igniting defendant resistance to inspection and delay in production.” Both proved accurate. The filing of books and records actions increased dramatically, as inspection appeared to be the only means of pleading a viable breach of fiduciary duty claim; defense firms complained about the epidemic of books and records actions; and defendants stridently refused to produce any documents in books and records under tenuous theories (that have since been rejected but continue to be asserted).

From the perspective of a neutral observer, it appears that stockholders’ use of 220 actions to investigate and diligence potential breaches of fiduciary duty has been a boon to the jurisdiction -- at least to the extent that the jurisdictional ideal is that legitimate breach of fiduciary duty claims be discovered and non-meritorious claims be ferreted out at an early stage. TCD was initially troubled by the procedurally warped and perhaps unprecedented pleading requirement imposed by Solera. But if the proof of the pudding is in the eating, certainly as compared with the types of breach of fiduciary duty actions that were being filed in the Court of Chancery between the time we began publishing in 2012 and the time of Solera and Fresh Market, TCD perceives breach of fiduciary duty actions that have been brought by plaintiffs who have obtained inspection of books and records as being far more often based on legitimately questionable activity, and as asserting appropriately litigable claims.

As with the Fresh Market matter, complaints based on evidence obtained through books and records actions have also revealed how easily nominal compliance with procedural requirements that deactivate judicial scrutiny under M&F Worldwide and Corwin can be given the “patina of normalcy” described by Vice Chancellor Laster in In re Del Monte Foods Co. Shareholders Litigation, C.A. No. 6027-VCL (consol.), opinion (Del. Ch. Feb. 14, 2011), which can sometimes only be “disturbed by discovery.” Chancellor Allen noted the same phenomenon in In re Fort Howard Corp. Shareholders Litigation, C.A. No. *09991-CA, memo. op. (Del. Ch. Aug. 8, 1988). (“Rarely will direct evidence of bad faith — admissions or evidence of conspiracy — be available. . . . [The] “surface of events . . . in most instances, will itself be well-crafted and unobjectionable.”)

In Nicholas Olenik v. Frank A. Lodzinski, et al. and Earthstone Energy, Inc., No. 392, 2018, opinion (Del. Apr. 5, 2019), the Supreme Court reversed the Court of Chancery’s dismissal of an action challenging a merger based on standard-of-review shifting under M&F Worldwide, finding that a controller had already negotiated economic terms of the transaction without board knowledge or approval before the controller purportedly conditioned the transaction “ab initio” on approval by an independent committee.

But as stockholders began in earnest to use the “tools at hand” -- which Delaware case law had for decades encouraged stockholders to use to investigate claims -- to expose genuine malfeasance and assert valid claims, the Supreme Court in KT4 Partners, LLC v. Palantir Technologies, Inc., No. 281, 2018, opinion (Del. Jan. 29, 2019) imposed limitations on information that stockholders could obtain under Section 220. Although the Palantir Court found that the stockholder plaintiff was entitled to inspection of informal communications among directors, including email, that was only because the board operated informally. The Palantir Court held that “the Court of Chancery should not order emails to be produced when other materials (e.g., traditional board-level materials, such as minutes) would accomplish the petitioner's proper purpose,” which notably would exclude evidence of deceitful or surreptitious conduct such as that found to defeat standard-shifting defenses in Fresh Market and Earthstone.

The issuance of Palantir seemingly prompted companies that had not exercised formality to retroactively correct course, for example by creating minutes for meetings long past -- presumably reflecting a desired narrative -- for production in response to books and records demands, perhaps (one might suspect) in an attempt to defeat the stockholder’s demand for entitlement to inspection of contemporaneous informal records that would reveal more troubling underlying conduct. And going forward, Palantir invited tactical creation of tailored contemporaneous board materials. While it is not apparent to TCD that companies immediately grasped the concept, facts alleged in In re Zendesk, Inc. Section 220 Litigation, C.A. No. 2023-0454-BWD (coord.), final report (Del. Ch. Aug. 25, 2023), for example, seem to suggest that counsel meticulously advised and papered board actions leading up to the sale of a company -- completed after acceleration of stock-option grants to key executives at a price 40% lower than an offer the board had rejected as inadequate four months earlier -- and there, the Magistrate in Chancery recommended that plaintiffs be entitled to inspection only of official board materials.

Soon after the issuance of Palantir, prominent Delaware corporate law scholars published Understanding the (Ir)Relevance of Shareholder Votes on M&A Deals (Thomas; Cox; Mondino). As discussed in TCD’s February 15, 2019 edition, the study undertook a detailed empirical examination of stock ownership and voting by institutional investors (particularly index funds), as well as arbitrageur acquisition of target-company shares from longer-term investors and other phenomena, and concluded that:

[T]he Delaware courts need to rethink their obsession with the shareholder vote, renounce the current doctrinal trends that are taking them in the wrong direction, and return to their historic role of evaluating whether directors have satisfied their fiduciary duties in M&A transactions.

(The same edition discussed Farewell to Fairness: Towards Retiring Delaware's Entire Fairness Review(Licht), which argued that M&F Worldwide’s move toward elimination of the entire fairness standard of review is “highly desirable in principle,” assuming that the integrity of stockholder voting is ensured “by securing the supply of full information throughout the process and minimizing the impact of potential conflicts.”)

At some point, TCD encountered the term “MFW creep.” Given the foregoing, if we were to guess what the term meant, we would guess that it referred to the Court’s deactivation of its own ability to consider breach of fiduciary duty claims in favor of purported stockholder self-determination, and the rather creepy subsequent developments that have moved away entirely from the rationale highlighted in In re Cox Communications of protecting stockholders (“. . . [A] relatively modest alteration of Lynch would do much to ensure . . . integrity [of the representative litigation process that is important to our corporate law's ability to protect stockholders against fiduciary wrongdoing], while continuing to provide important, and I would argue, enhanced, protections for minority stockholders. . . .”) to protecting corporate defendants from litigation costs, settlement value, appraisal, and discovery through the tools at hand -- even in the face of evidence that corporate controllers, insiders, and fiduciaries intentionally lie, mislead, and feign compliance with standard-shifting requirements in order to expropriate corporate value for themselves with impunity.

TCD’s guess does not accurately capture what “MFW creep” is understood to mean, however. In Optimizing the World's Leading Corporate Law: A 20-Year Retrospective and Look Ahead (Hamermesh; Jacobs; Strine), the authors urged that Delaware case law had misapplied “MFW” by finding that conflicted controlling stockholder transactions other than freeze-out mergers are subject to standard shifting from entire fairness to business judgment only if conditioned on approval by both an independent special committee and unaffiliated stockholders, and argued that standard shifting should apply outside the freeze-out context if only one such protection is provided.

It was against this backdrop that the Match Group case arose. In In re Match Group, Inc. Derivative Litigation, C.A. No. 2020-0505-MTZ (consol.), memo. op. (Del. Ch. Sept. 1, 2022), the Court dismissed stockholder claims challenging a reverse spinoff and merger in which a conflicted controlling stockholder allegedly obtained non-ratable benefits. The Court found that, because the transaction was approved by a special transaction committee and by stockholder vote, those protections shifted the entire fairness standard of review to business judgment under M&F Worldwide. Plaintiffs appealed, in part arguing that the Court erred in finding that the special committee (which included a member who was not independent of the controlling stockholder) was independent for purposes of M&F Worldwide. Defendants responded that, because the challenged transaction was not a squeeze-out merger, the trial court erred by finding that both approval by an independent committee and approval by stockholder vote were required to shift the standard from entire fairness to business judgment. Rather, they argued, either approval by independent directors or unaffiliated stockholders was sufficient to shift the standard.

Although defendants did not raise that issue before the trial court, the Supreme Court found that the issue should be considered in the interests of justice, and requested supplemental briefing on “whether the Court of Chancery judgment should be affirmed because the Transactions were approved by either of (a) the [transaction] Committee or (b) a majority of the minority stockholder vote[.]”

Today’s edition previews the parties’ arguments on appeal, as well as the arguments of three separate amicus curiae in support of plaintiffs: a group of current law professors; a former professor, who is also a current and former public company director (Charles Elson); and a venture capital fund. Defendants argue that either approval by a majority of independent directors, approval by an independent committee, or approval by unaffiliated stockholders is effective to shift the standard of review applicable to a conflicted controlling stockholder transaction other than a squeeze out merger from entire fairness to business judgment, that this has been the law for decades, that such standard shifting is required under 8 Del. C. § 144, and that it is also required by “MFW” due to its refutation of the inherent coercion doctrine. The law professors’ arguments focus on economics and agency costs associated with controlling stockholders, while Elson’s arguments challenge defendants’ interpretation of case law that is asserted to have provided for standard shifting, and the venture capital fund discusses its practical concerns as a stockholder about expropriation of company value by interested insiders.

TCD notes that, as has become customary with respect to the standard-shifting mechanism adopted by the Supreme Court in M&F Worldwide, the mechanism, the Court of Chancery Opinion adopting the mechanism, and the Supreme Court Opinion affirming the Court of Chancery Opinion are all referred to as “MFW” -- which to some degree complicates understanding of what is being discussed. To the extent “MFW” is described as having rejected the doctrine of inherent coercion, TCD does not understand how the Supreme Court’s Opinion in M&F Worldwide rejected the doctrine. To the extent standard shifting from entire fairness to business judgment has always been the law, TCD confesses that it understood standard shifting to be a novel procedure first proposed (in a judicial opinion) in In re Cox Communications and first applied in In re MFW -- and before that, the only “shifting” mechanism was burden shifting. TCD is quick to add that it hasn’t been around for decades and hasn’t seen it all.

On the other hand, we have been extremely attentive observers of Delaware corporate litigation since 2012, and to the extent standard shifting through a cleansing mechanism other than under those approved in M&F Worldwide and Corwin are accepted methods of venerable vintage, their application somehow escaped our notice for the last eleven years. Nor are we alone in apparently overlooking this point of law. The defendants’ supplemental reply brief in Match distinguishes at least four prior Supreme Court opinions (each stating that the use of a single cleansing device could have only a burden- (not standard-) shifting effect in the context of a conflicted, non-squeeze-out transaction with a controller), on the grounds that defense counsel in those cases had failed to raise the argument. An odd oversight, if this is, in fact, the traditional rule.

It also bears mention that in Alan Russell Kahn v. Tremont Corp., No. 170, 1996, opinion (Del. June 10, 1997), the Delaware Supreme Court explicitly rejected the IAC defendants’ position in a case involving a share purchase, not a squeeze-out. In reviewing de novo the proper standard of review, the High Court wrote broadly about “challenged transaction[s] involving self-dealing by a controlling shareholder” -- not merely squeeze-out mergers:

Ordinarily, in a challenged transaction involving self-dealing by a controlling shareholder, the substantive legal standard is that of entire fairness, with the burden of persuasion resting upon the defendants. [William B. Weinberger v. UOP, Inc., No. 58, 1981, opinion (Del. Feb. 1, 1983)]; See [Emanuel G. Rosenblatt, et al. v. Getty Oil Co., No. 352, 1983, opinion (Del. May 9, 1985)]. The burden, however, may be shifted from the defendants to the plaintiff through the use of a well functioning committee of independent directors. [Alan R. Kahn v. Lynch Communication Systems, Inc., et al., No. 272, 1993, opinion (Del. Apr. 5, 1994)]. Regardless of where the burden lies, when a controlling shareholder stands on both sides of the transaction the conduct of the parties will be viewed under the more exacting standard of entire fairness as opposed to the more deferential business judgment standard. Id.

Entire fairness remains applicable even when an independent committee is utilized because the underlying factors which raise the specter of impropriety can never be completely eradicated and still require careful judicial scrutiny. [Weinberger]. This policy reflects the reality that in a transaction such as the one considered in this appeal, the controlling shareholder will continue to dominate the company regardless of the outcome of the transaction. [Edith Citron v. E.I. Du Pont de Nemours & Co., et al., C.A. No. *6219-VCJ, opinion (Del. Ch. June 29, 1990)]. The risk is thus created that those who pass upon the propriety of the transaction might perceive that disapproval may result in retaliation by the controlling shareholder. Id.Consequently, even when the transaction is negotiated by a special committee of independent directors, "no court could be certain whether the transaction fully approximate[d] what truly independent parties would have achieved in an arm's length negotiation." Id. Cognizant of this fact, we have chosen to apply the entire fairness standard to "interested transactions" in order to ensure that all parties to the transaction have fulfilled their fiduciary duties to the corporation and all its shareholders. [Kahn]

With respect to 8 Del. C. § 144, TCD’s February 8, 2019 edition collects the sparse sum of references to the statute that this publication had encountered or discussed as of that date, to which we now add Anurag Mehta v. Mobile Posse, Inc., et al., C.A. No. 2018-0355-KSJM, memo. op. (Del. Ch. May 8, 2019). As with the decades of precedent providing for standard shifting, to the extent Section 144 requires standard shifting in controlling stockholder transactions, litigants seem not to have found occasion to raise it for the past decade. The plain language of that statute addresses the use of cleansing mechanisms to prevent voidness of transactions with interested directors and says nothing about controlling stockholders, and given that void acts reside outside the realm of equity -- as the Supreme Court ruled in CompoSecure, LLC v. CardUX, LLC, No. 177, 2018, opinion (Del. Nov. 7, 2018), and recently reaffirmed in Gregory A. Holifield, et al. v. XRI Investment Holdings, LLC, No. 407, 2022, opinion (Del. Sept. 7, 2023) -- TCD finds it difficult to conclude that Section 144 governs application of equitable standards of review.

Generally, TCD perceives the defendants’ arguments as being reliant upon overstatement of already attenuated principles, and finds the plaintiffs’ and the amici’s analyses of the law, the economic and policy consequences, and the practical consequences to stockholders -- of what would be effectively the elimination of judicial review of conflicted controlling stockholders’ actions (given the ease with which purportedly-independent approval can be procured) -- comparatively more cogent and more compelling. We will not attempt to offer our own take on the points they make, but follow their focus on practical rather than merely theoretical constructs, noting that the idea that inherent coercion does not exist is difficult to square with reality. It is inconsistent with the response observed all-too-often from corporate directors whose positions are threatened by activist stockholders: capitulation to all demands.

Why directors would be less protective of their positions when threatened by a controlling stockholder than by an activist stockholder is difficult to imagine. And we assume it is the rare and fortunate individual who has never felt or responded to at least a tacit threat to their position or their livelihood in a manner with which they are not entirely comfortable. It is still more difficult to disregard detriments to minority stockholders of controlling stockholder expropriation. The very notion of M&F Worldwide’s standard-shifting protections, by requiring controllers to disable themselves, recognized the reality of that threat. Current market realities -- in which control disproportionate to economic interest is conferred through super-voting stock -- seemingly increase, rather than reduce, legitimate concerns of expropriation. Whatever past case law supposedly can be read to suggest, practical considerations do not seem to cry out in favor of abandoning judicial scrutiny.

Nevertheless, TCD interprets the Supreme Court’s agreement to consider defendants’ argument in the disfavored context where it was never raised before the Court below as indicative of amenability to the position. TCD does not have an admirable track record for predicting what the Supreme Court will do -- but the Court seemed to take pains to remand and reconsider Marion Coster v. UIP Companies, Inc., et al., No. 163, 2022, opinion (Del. June 28, 2023) on issues that did not figure prominently in the trial court’s decision -- perhaps for the purpose of constraining application of equity review under Andrew H. Schnell, Jr., et al. v. Chris-Craft Industries, Inc., opinion (Del. Nov. 29, 1971), only to cases involving stockholder voting -- and to raise the issue of voidness not argued before the trial court in CompoSecure for the purpose of precluding application of equity (and to reaffirm that analysis in XRI). This appears to be in connection with an increasing embrace of Delaware corporate law as a corpus governed by contract principles, antithetical to equity, with the object of conferring greater certainty and holding parties to things-deemed-agreements. This is mere speculation, however; we are unaware of any clear statement by members of the Supreme Court about such an intent. But if that is the intent, TCD questions what the effective elimination of equitable judicial review of controlling stockholders’ interested transactions leaves of equity’s role in Delaware law beyond a smoldering crater.

As noted at the beginning of this discussion, TCD regards Delaware’s unique application of equity as what distinguishes the jurisdiction and fosters the franchise. Perhaps reasonable minds could disagree on that point; if so, we hope they are correct. On this point, we find Professor Elson’s assessment worthy of emphasis:

The IAC Defendants seek a rule that is a gift to controllers at the expense of minorities, plain and simple. The IAC Defendants would have Delaware take a giant leap in the direction of the overly permissive legal regime of Nevada (which has effectively abandoned entire fairness review) -- the classic “race to the bottom.” That is not the right path for Delaware. Delaware should protect all investors, not simply controlling ones as Defendants’ rule would enable. . . .

. . . More importantly, the existing doctrine has not proved unworkable. For all the reasons set forth above, the IAC Defendants’ arguments to upend the entire fairness doctrine as applied to non-squeeze-out conflicted-controller transactions are not even marginally compelling, let alone urgent or bespeaking clear error. As amicus has observed [in Why Delaware Must Retain its Corporate Dominance and Why it May Not(Elson)], “Delaware’s preeminent role in corporate regulation has endured, despite numerous challenges, for decades [because] . . . [i]nvestors, directors, and managers respect its even-handedness and predictable approach to regulation and the resolution of corporate controversy. This is the product of a highly advanced corporate code and a judiciary renowned for its neutrality and corporate specialization.”

Put simply, Delaware law is working. The Delaware franchise is strong, and the Delaware brand is more valuable than ever. Accepting the IAC Defendants’ invitation would do far more harm to the franchise than any theoretical concerns about the Court of Chancery being unable to weed out nuisance claims, even if they are viewed under the entire fairness paradigm. Delaware’s reputation is based on maximizing stockholder value and, to achieve that goal, it has carefully managed the balance between enabling transactional flexibility and ensuring investor protection. The IAC Defendants’ proposed approach would undo that careful balance and send the law in precisely the wrong direction.

The Court should not try to fix what is not broken. Change and adaption are inevitable and desirable. But when change happens, it should be through gradual tweaks at the margins through the familiar, common-law approach that is at the core of Delaware’s brand. This Court must not perform the radical and dangerous surgery that the IAC Defendants demand.

Chonky and in depth boy. Going to have to set down and give it the full attention it deserves after work.

Chance, I studied under Professor SUSAN Wachter. The time in class serves me well to.rhis day.